CSM Technologies IPO: GovTech Moat Meets Stretched Payment Cycles

Evaluating the growth outlook, niche domain depth, and operational metrics of an established e-governance solutions provider.

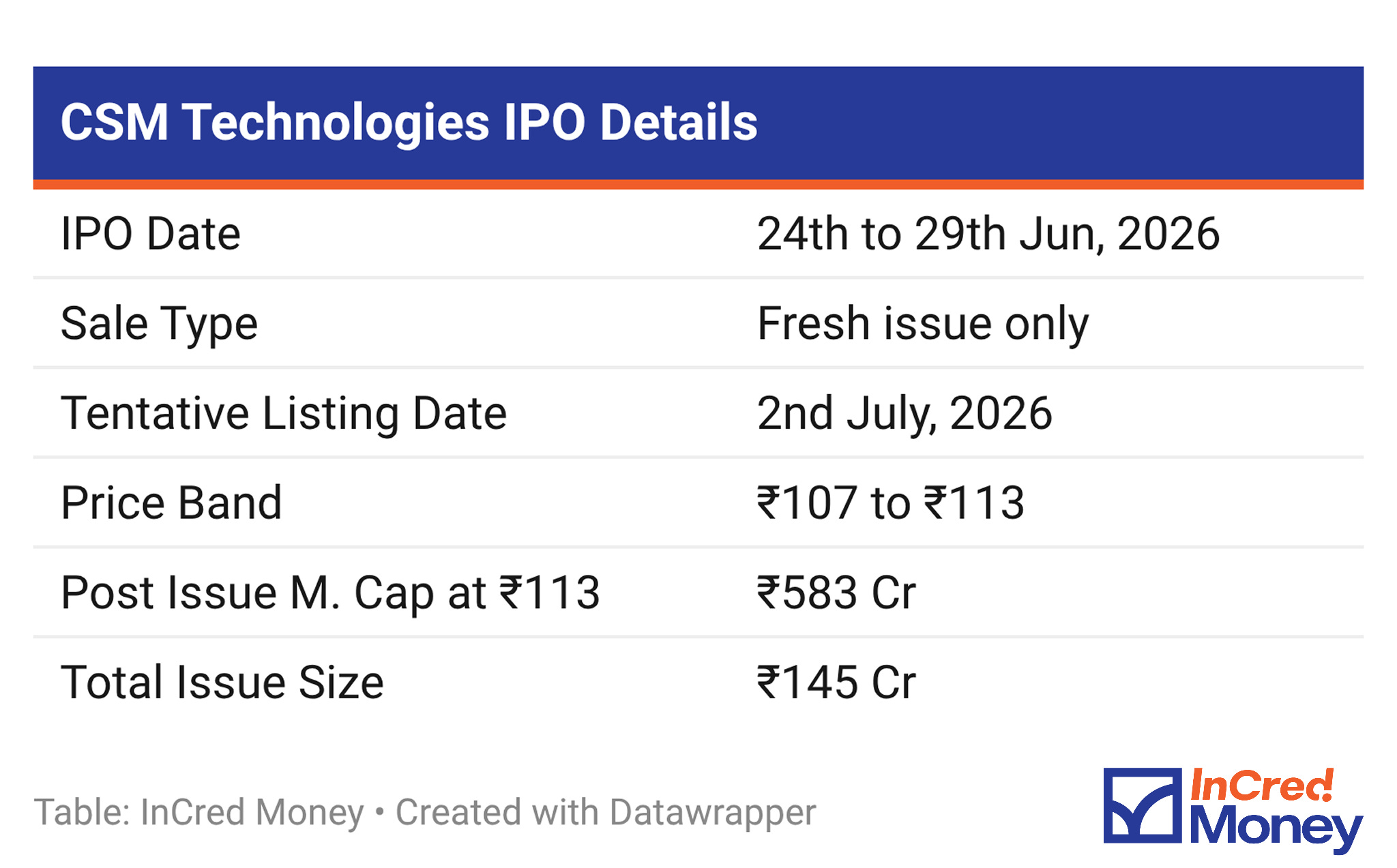

CSM Technologies Limited, is launching a ₹146 Cr IPO on June 24, 2026. CSM has built e-governance platforms and digital infrastructure from its Bhubaneswar campus since 1998 and its core system controls the tracking of roughly 80% of India’s major mineral output.

IPO Summary

For ABCs on all upcoming IPOs, subscribe to IPOs with InCred Money

Continue reading!

The Big Picture

The global Information Technology and IT-enabled Services (IT-ITeS) sector is currently riding a massive wave of digital transformation. Businesses and governments alike are rapidly adopting cloud computing, which enhances efficiency, customer experiences, and innovation.

The Indian government’s spending on IT and digital initiatives is projected to grow at a steady CAGR of 7.2% from FY26E to FY31P, rising from USD 1.12 billion in FY25 to USD 1.74 billion by FY31P

This growth is being driven by the public sector’s urgent need for e-governance platforms, smart city solutions, and automated public service delivery.

Business Model Explained

Every Indian state government that wants to collect mining royalties more efficiently, admit students to government colleges, or route welfare payments to the right bank account needs one thing before anything else: working software.

For twenty-seven years, CSM Technologies has been building exactly that, from a campus in Bhubaneswar’s Infocity.

The company designs, deploys, and maintains the digital infrastructure of Indian governance.

CSM participates in open competitive tenders floated by state governments, central ministries, PSUs, and development agencies.

The company wins roughly half of what it bids on: its bid-to-win ratio has averaged 0.52 over the past three years.

Once a contract is awarded, and the project is delivered, maintenance and operations contracts often extend the relationship for years, generating lower-margin but predictable income.

In its journey so far, they have executed projects across 20 cities in India and 14 countries internationally.

The company is amongst the few IT solutions companies, who have delivered first of its kind projects for government as well as for the private sector whilst serving a diverse sector

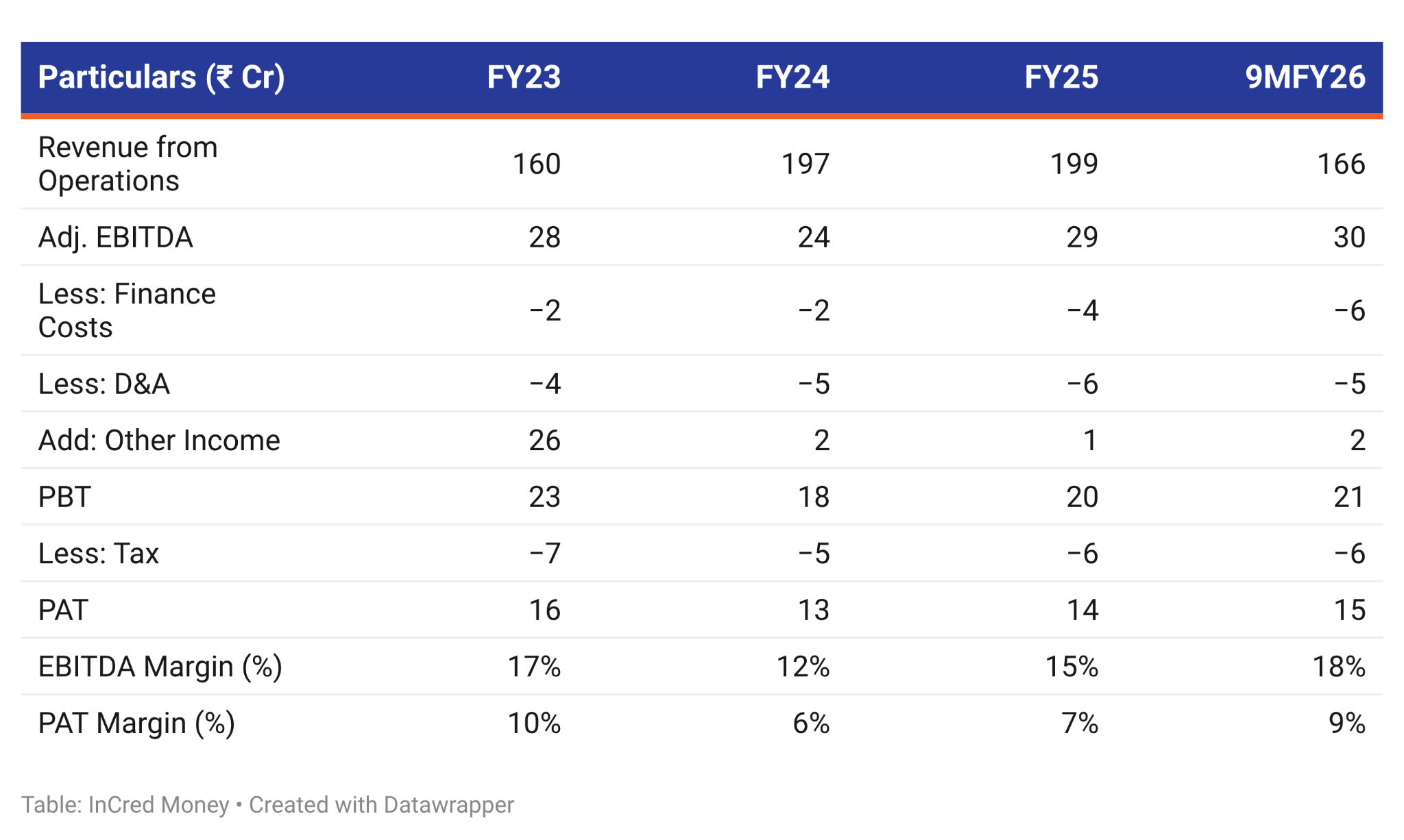

From Revenue to the Bottom Line

CSM Technologies exhibits robust top-line momentum, scaling revenue from ₹160 Cr in FY23 to ₹199 Cr in FY25, driven by sustained GovTech demand.

However, its government-heavy client base makes the business highly working-capital intensive. Extended public sector payment cycles have nearly tripled finance costs (from 2.12 to 6.20) as short-term bank borrowings were utilised to bridge cash flow.

Crucially, CSM intends to use the IPO proceeds to prepay this debt and fund working capital needs a move that should directly alleviate interest burdens and unlock substantial bottom-line profitability post-listing.

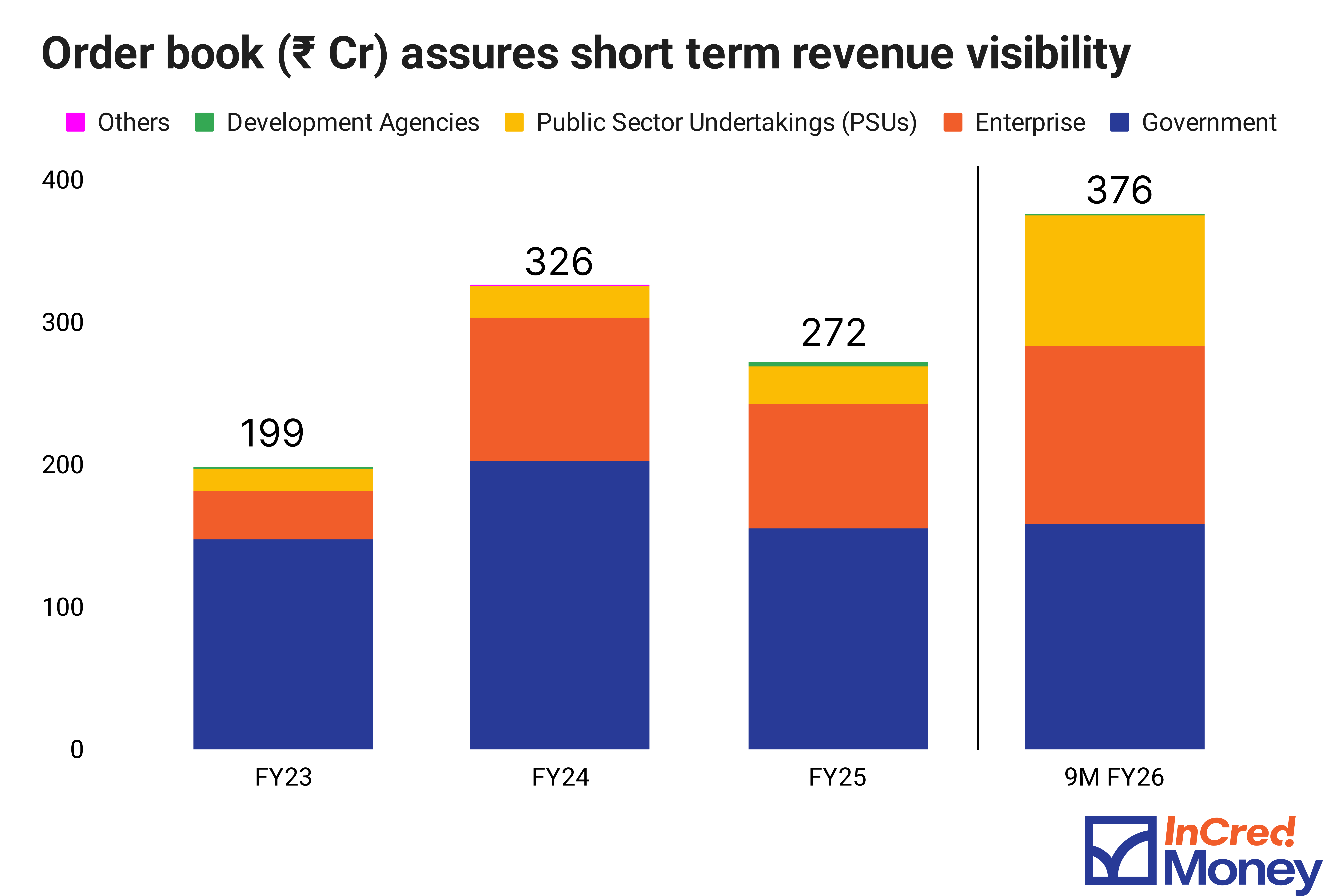

Operating Metrics and How They Are Moving

The order book peaked at ₹376.40 Cr in 9M FY26. At nearly 1.9x the total revenue of FY25, this backlog provides highly reasonable near-term visibility.

(Source: RHP)

Receivable days are the biggest red flag. They have stretched from 55 days in FY24 to 129 days in 9MFY26, driven by milestone billing and slow government payment cycles. The company expects this number easing toward 100 days in FY28.

(Source: RHP)

What the company is doing to improve

Proprietary platform investment: CSM’s Low Code No Code (LCNC) framework and AI Model Orchestration Platform are intended to reduce per-project build costs and shorten go-live timelines for government projects.

EMTECH unit: An internal incubation lab piloting AI voice bots, computer vision, and generative AI tools, with intent to embed these in live government projects.

Geographic expansion: Exploring new geographies like Kenya and Ethiopia.

M&A pipeline: Board-approved strategy to acquire capabilities in cybersecurity and CRM. No targets identified yet.

Peer Comparison (FY25)

(Source: RHP)

CSM has no exact listed peer in India. Trigyn Technologies and Allied Digital Services operate at four to five times CSM’s revenue and have fundamentally different models.

When benchmarking CSM Technologies against its listed peers, a fascinating narrative emerges: bigger does not always mean more profitable. While companies like Trigyn Technologies and Allied Digital Services boast massive top-line revenues, CSM Technologies shines where it matters most to investors—margins and capital efficiency

Valuation

(Source: RHP, Screener)

(Annualised P/E has been used for CSM Technologies)

Key Risks

1. The business has not scaled meaningfully in 27 years

CSM was incorporated in 1998. It posted revenue of ₹199 Cr in FY25. That is a long time to still be a sub-₹200 Cr business. The model is structurally constrained: every contract requires a competitive tender win, project execution spans months to years, and government payment cycles slow cash conversion.

2. Top 3 customers account for 40% of revenue

In the nine months ended December 2025, CSM’s top 3 customers contributed 40.6% of revenue. The top 10 customers contributed 69.6%. Contracts are won through competitive tender, which means there is no guarantee any individual customer renews or awards new work. Government clients can terminate contracts, reduce scope, or simply not issue fresh tenders.

3. Mining is the core vertical and carries sector-specific risk

Mining and Allied Services is CSM’s largest revenue segment at 24.7% of FY25 revenue, and the company’s most defensible intellectual property sits here: its Integrated Mines and Minerals Management System (i3MS) is the operating platform for Odisha, Jharkhand, and Chhattisgarh, which together account for roughly 80% of India’s major mineral output. But this concentration cuts both ways. A policy change in any of these states or a regulatory dispute would directly hit CSM’s top line and order book.

Conclusion

CSM Technologies features a resilient business model with deep domain expertise in the GovTech space with sticky government contracts.

However, its heavy reliance on public sector clients introduces a structurally intensive working capital cycle, characterised by extended receivable days. Tracking the company’s post-listing financial performance and cash flow data over the next few quarters will provide clearer visibility into whether these payment cycles can normalise sustainably.

Disclaimer

Any video/image/text content is for educational and informational purposes only and does not constitute financial advice. Please do your own research or consult a qualified financial advisor before making any investment or trading decisions. Trading in stock markets involves the risk of loss.

Investments in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

InCred Money Broking Limited : NSE Member Code 09073, BSE Member Code 6329, MCX Member Code: 55215 , NCDEX Member Code : 1233 NSDL : IN-DP-474-2020 . SEBI Registration No. NZ000164738

Compliance Officer: NSE,BSE,MCX,NCDEX,NSDL : Mr RK Jain , 011-40409999 support@stocko.in

Registered Office:- 3rd Floor, Building No.5, Local Shopping Complex, Rishabh Vihar, Near Karkarduma Metro Station. East Delhi – 110092