Decoding GSP Crop Science Limited IPO

The Macro Context

India is a majorly agrarian nation. One of the major issues the agriculture sector faces is the loss of an estimated ₹90,000 Cr annually to pests, weeds, and fungal diseases, a significant portion of total agricultural output. Despite this, per-hectare agrochemical consumption in India sits less than a fifth of China’s consumption levels. However, China still accounts for a huge percentage of India’s insecticide and herbicide imports. This imbalance between consumption and reliance on imports is a problem as well as an opportunity for Indian agrochemical manufacturers, and is also the incentive that GSP Crop Science is positioned to capture.

GSP’s IPO consists of a fresh issue of ₹240 Cr and ₹160 Cr of Offer for Sale , totaling to a total issue size of ₹400 Cr. Proceeds will be used to fund working capital and general corporate purposes.

Agrochemical industry: the push towards self-reliance

There’s two types of product lines that make up a company like GSP’s portfolio:

Technicals, are the concentrated, purified active ingredients responsible for killing the pests, fungi or weeds. They are sold primarily B2B, to other manufacturers who blend them into end-use products. Up until recently, technicals’ registration was encouraged but not mandatory.

Formulations are the final product farmers buy. A formulation takes a technical active ingredient and combines it with solvents, emulsifiers, and stabilizers, then packages it for field application. Formulations mandatorily require registration. A company that can hold patents on novel formulations has unparalleled advantage over rivals.

GSP’s strategic story is the migration of its revenue mix from technical toward formulations:

Understanding its business model

Founded in 1985 as Gujarat Superphosphate Industries, GSP Crop Science is a leading agrochemical manufacturer. It produces insecticides, herbicides, fungicides, and plant growth regulators as both Formulations and Technicals.

GSP holds 10 exclusive patented formulations which no other Indian company can replicate. Examples include Platform (wheat herbicide) and Raavan (rice insecticide).

GSP is also among the first indigenous manufacturers of technical grade actives. Their technicals are sold to top agrochemical companies like Bharat Rasayan Limited, Willowood Chemicals, Indogulf Cropsciences, etc.

GSP operates 5 facilities located in Gujarat and Jammu & Kashmir. The J&K facility benefits from the J&K budgetary support scheme under GST in the form of 58% of CGST and 29% of IGST refunds.

Operational KPIs

Formulations Revenue Mix: Formulations went from 59% in FY23 to 72% in H1FY26. This is the central driver that has helped improve its margins.

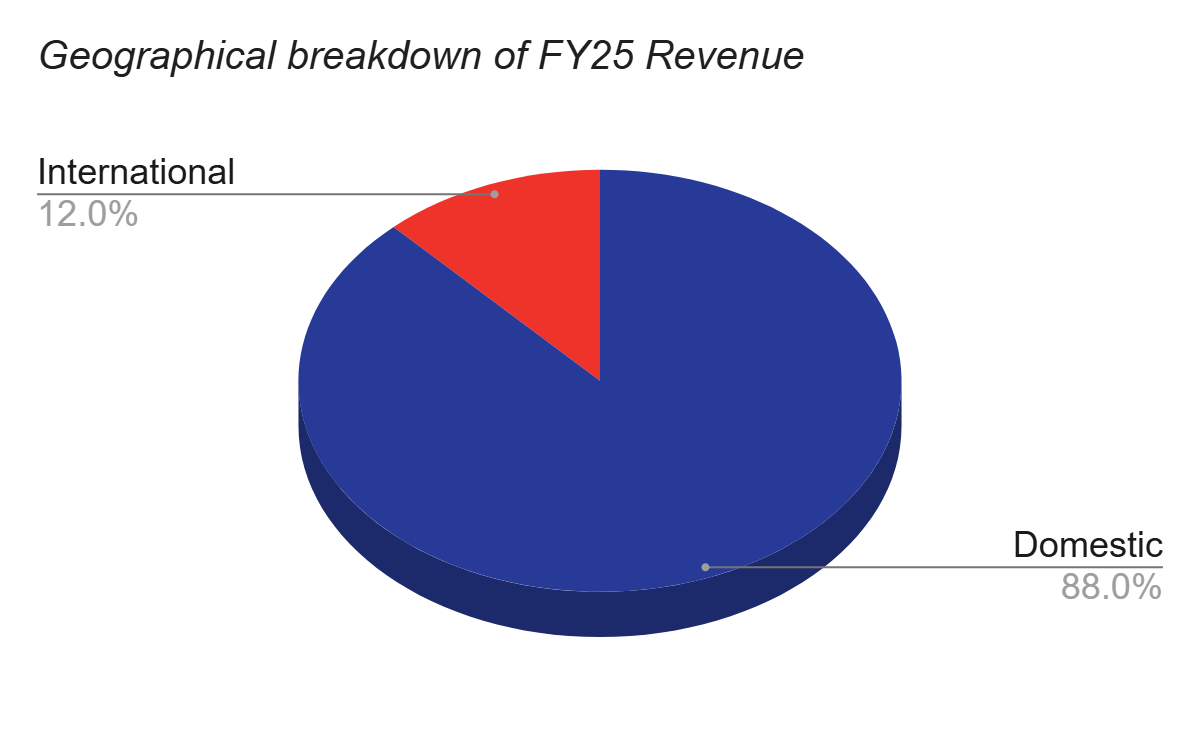

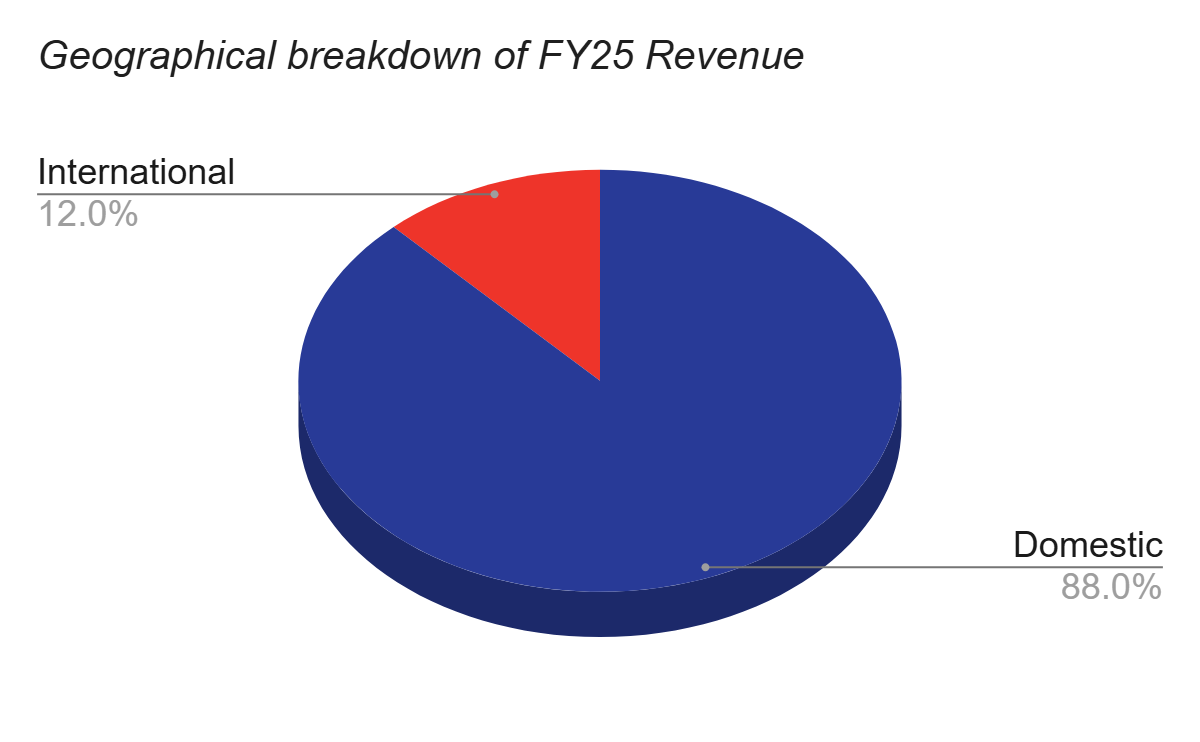

88.8% of revenue came from domestic sources in FY25. Internationally, revenue comes from 37 countries, primarily Uruguay, USA, Vietnam, and Brazil. In fact, GSP acquired a Brazilian subsidiary (GSP Agroquimica Do Brasil LTDA) in 2023 to anchor Latin American growth.

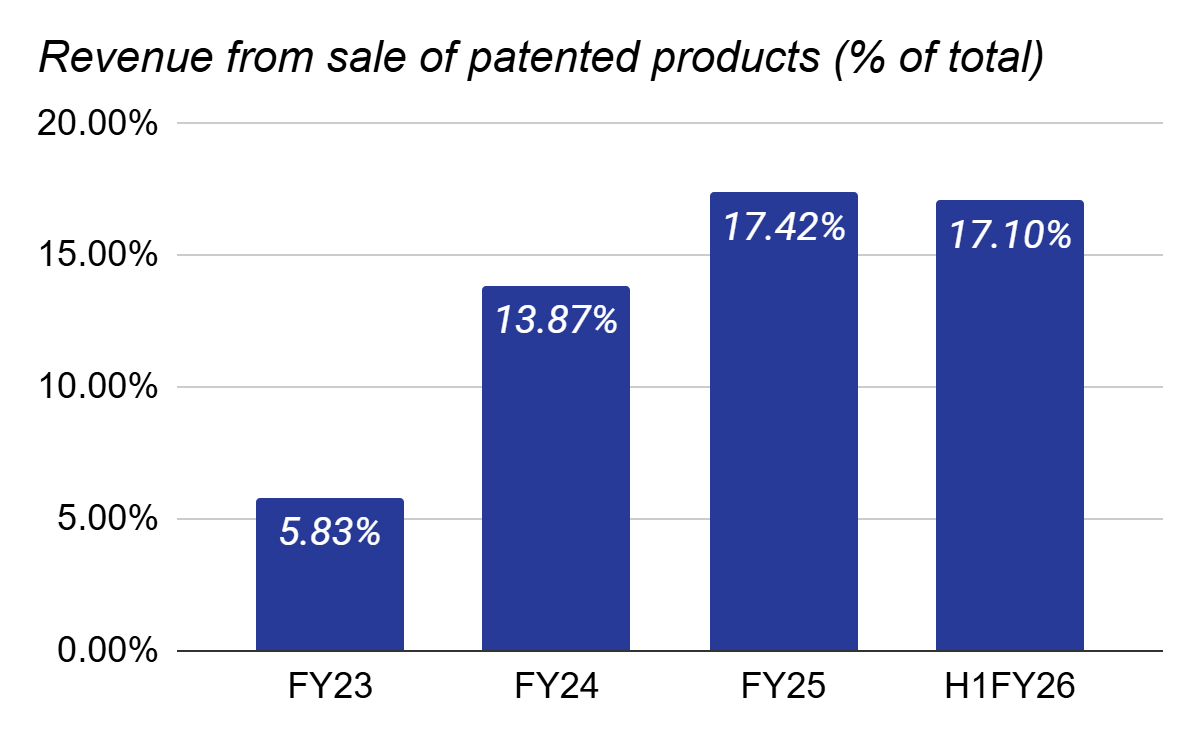

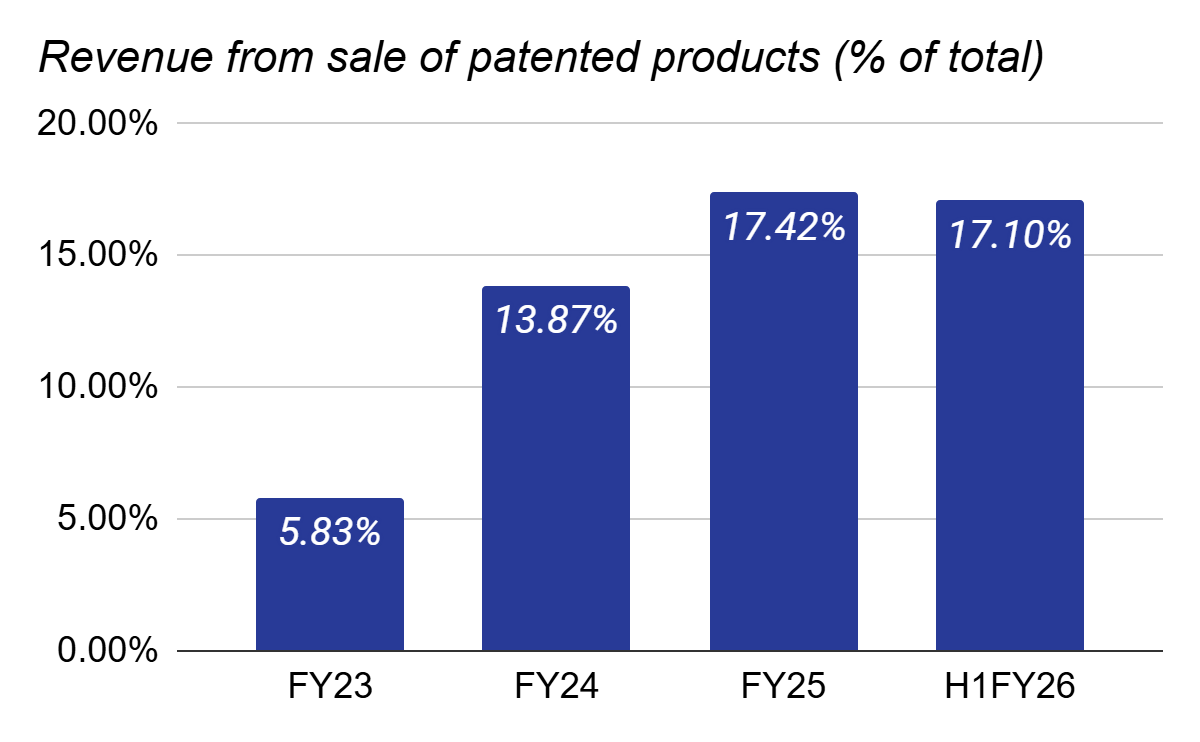

Twice as much revenue has already been generated from the sale of patented products in H1FY26 as it was in FY23. Sale of patented products is a stable source of revenue, though its share is still only about 1/5th of all sales.

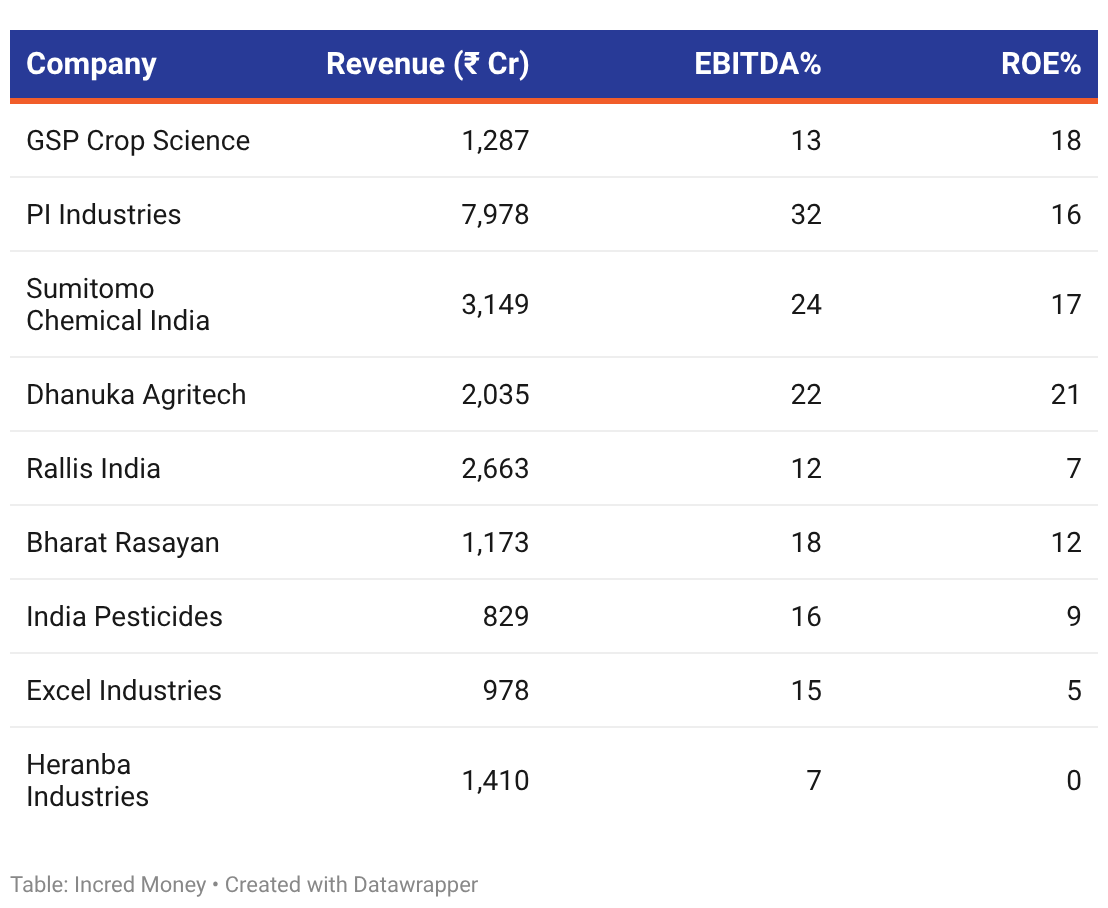

Peer Comparison — FY25

GSP’s EBITDA margin is underwhelmed by most peers. At GSP’s current scale and mix, a fair comparison is Bharat Rasayan. The margin gap here is partly explained by GSP’s higher Technical segment share, which has lower margins than Formulations.

GSP’s ROE of 18.38% is the highest in the peer set shown. Note that this is partially a function of a smaller net worth base vs. much larger capital bases at PI Industries or Rallis.

Financial Analysis

Revenue declined 4.25% in FY24 due to the decline in product prices.

PAT Margin (%) PAT margin expanded by 9% in about 3 years. This is accompanied by lower finance costs, lower costs of materials consumed in FY24 and FY25.

Finance costs fell from ₹37 Cr in FY23 to ₹31 Cr FY25 despite the business growing, reflecting debt repayment in FY24. Debt/Equity ratio in the same time also improved from 0.77x to 0.58x.

Risk Analysis

Raw material dependence on China: GSP sources more than a third of their materials and intermediates from China. Geopolitical trade friction can compress margins sharply and quickly, as seen in the FY22/23 cost spike where material costs hit 72.7% of revenue.

Working capital intensity: 117 NWC days in FY25 mean that each ₹1 of additional annual revenue requires roughly ₹32 Paise of additional working capital. The business is inherently capital-intensive, and the ₹240 Cr fresh issue is entirely directed at this need.

Conclusion

GSP Crop Science is a 40-year-old agrochemical company shifting from a Technicals heavy business to a Formulations led one. The fact that this IPO funds working capital rather than building new competitive moats for example, investing in assets, is something to look out for.