India's Third-Largest Basmati Brand Is Going Public! Inside ACJKEL IPO

India supplies 75% of the world's basmati rice, and most of it passes through brands you've never seen on a supermarket shelf. ACJKEL exports to 38 countries through a 40-year-old brand. 52% revenue CAGR, 431 domestic distributors, and a ₹440 Cr IPO.

The Macro Context

India recorded a 16% volume increase in the export of basmati rice in FY25 over the prior year. The Middle East (Saudi Arabia, Iran, Iraq, UAE) accounts for the bulk of shipments. In fact, India supplies roughly 75% of the world’s basmati rice.

With a Geographical Indication (GI) tag protecting Indian basmati’s identity in international markets, pricing power has improved vastly.

The domestic side is equally compelling. India’s per-capita rice consumption remains high, and urbanisation is driving a shift from loose/unbranded rice to packaged, branded variants. Branded basmati is bought at a big premium over unbranded rice.

Amir Chand Jagdish Kumar (Exports) Limited (ACJKEL) is going public precisely to ride this wave. This IPO is completely a fresh issue of ₹440 Cr, allocated entirely towards working capital.

The Difference Between Commodity Rice and Branded Basmati

Commodity rice trading involves buying paddy/rice and selling it in bulk, often to middlemen or institutional buyers. Margins are thin, volumes are the only lever, and price discovery usually happens in mandis.

Branded basmati processing adds three layers of value:

1) milling and ageing

2) brand and SKU architecture

3) distribution depth.

Basmati processing creates higher margins than unbranded commodity rice.

ACJKEL operates in branded basmati, with both domestic and export channels. What makes its current phase interesting is a deliberate pivot from export-led to domestic-led revenue.

Understanding the Business Model

ACJKEL is a fully integrated basmati rice company: it procures paddy primarily from Punjab and Haryana through 325 registered procurement agents across mandis, then mills it across three facilities in Amritsar, Jind, and Delhi, before aging and packaging it for sale.

ACJKEL sells through a distributor network of domestic and international distributors, selling across 38 countries.

The flagship brand ‘AEROPLANE’ launched over 40 years ago.

It consists of a portfolio of 40+ sub-brands such as Aeroplane La-Taste, Aeroplane Classic, Ali Baba, World Cup, Jet, etc.

The goal here is to target different price segments: Premium, Medium, Value, and HORECA (Hotel, Restaurant and Cafe). The company also holds 100 registered trademarks domestically and internationally.

ACJKEL is also expanding into FMCG staples (atta, maida, besan, sooji, salt, sugar) leveraging the Aeroplane brand.

Operational KPIs

An important KPI has to do with the fact that ACJKEL is aiming for further expansion in the domestic market. This can be seen in its rapidly rising domestic revenue as a portion of its total revenue base.

Capacity Utilisation: Utilisation has improved driven by higher domestic sales volumes.

Distributor Network: 431 distributors in India and 53 outside India as of Feb 2026. This expansion underpins the domestic revenue growth story more feet on the street translates directly into shelf presence in Tier 2/3 markets.

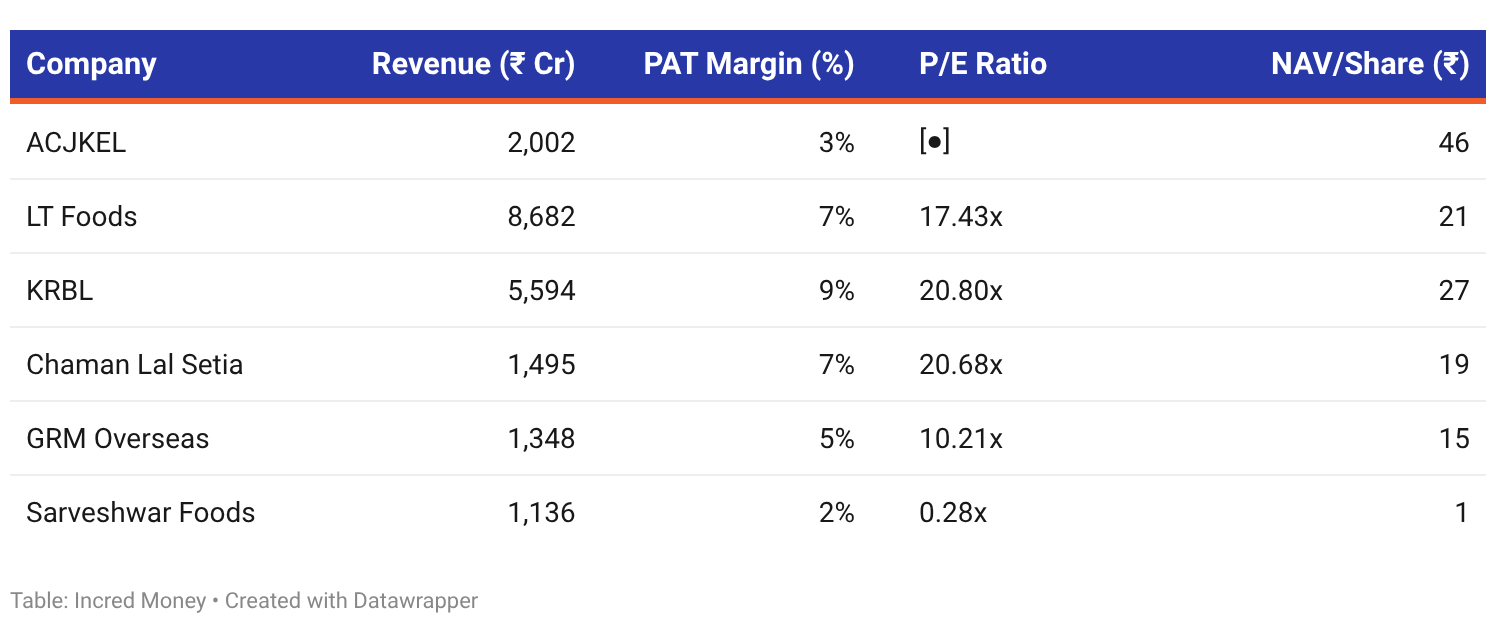

Peer Comparison

ACJKEL ranks 3rd by revenue among listed peers. It’s interesting to note that unlike others, ACJKEL has built its scale predominantly through distribution breadth and promoter relationships rather than advertising spends.

At 3.04%, ACJKEL’s PAT Margin is below almost all peers. One of the reasons for this is high finance costs. However, as domestic branded revenue scales further, margins should improve.

Financial Analysis

Revenue grew at a 52.1% CAGR from FY23 to FY25. Volumes grew 55.5% over the same period, specifically domestically. The key strategic shift is domestic-led growth. Domestic revenue has grown because the company has deliberately built up its domestic distribution network, while trying to maintain its international sales.

Finance cost is a sizable profitability constraint, driven by working capital borrowings for seasonal paddy procurement. The IPO proceeds should partially reduce this burden.

PAT Margin saw a 3.5x increase in the past two years. The key variable for PAT this year would be whether finance cost reduces post-IPO listing.

Risk Analysis

Debt is the defining risk: D/E of 2.07x in FY25 is the highest leverage ratio in its peer set.

Pakistan competition: Pakistan is a direct competitor in export markets. Pakistani rupee depreciation has made their rice more price-competitive, particularly in Iran, which is historically India’s largest export market.

Customer and distributor concentration: Top 10 customers represent 45% of H1FY26 revenue. The loss of even two or three large distributors or institutional buyers could create a revenue gap.

Conclusion

ACJKEL is a credible branded basmati player with a clear strategic direction to build domestic branded Basmati revenue. But the financials reflect a business still in transition. Its profits are contingent on finance costs falling, which depends on the IPO proceeds being deployed effectively.

(Disclaimer: Any video/image/text content is for educational and informational purposes only and does not constitute financial advice. Refer - https://stocko.in/stocko-disclaimer/.

Above information is taken from RHP filings available on https://www.sebi.gov.in/. Please do your own research or consult a qualified financial advisor before making any investment or trading decisions. Trading in stock markets involves the risk of loss.)