All About That Bling: The Advit Jewels Limited IPO

This company preserves an age-old tradition of handcrafting beautiful gem studded jewellery. Read all about their IPO

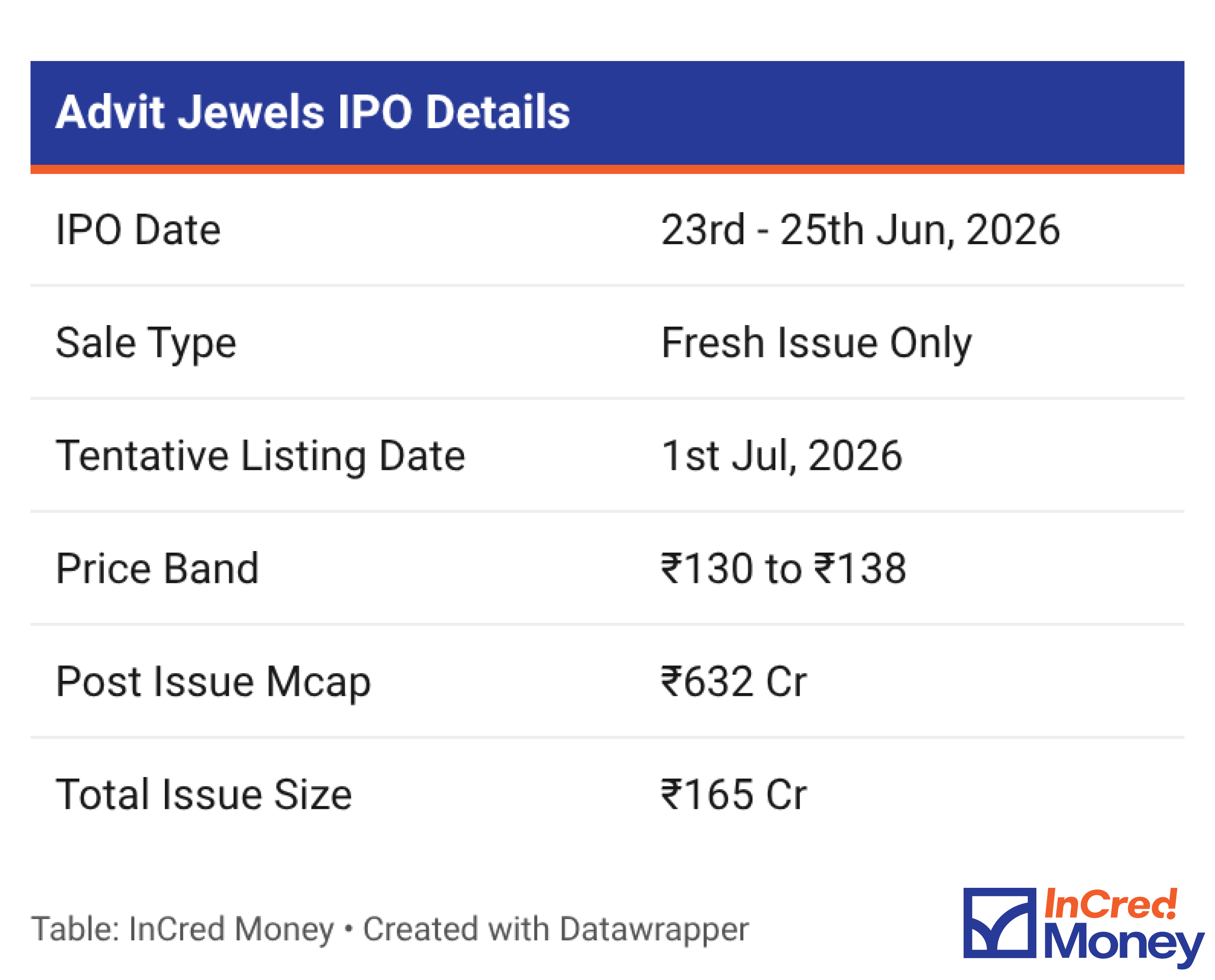

Advit Jewels is filing a ₹165 Cr IPO on June 23, 2026. Advit Jewels, based in Jaipur, Rajasthan, is a seller of Kundan Polki jewellery, and sells majorly to B2B clients with B2C sales making a smaller portion of revenue. Below is a breakdown of their IPO and business.

Advit Jewels IPO Summary

For ABCs on all upcoming IPOs, subscribe to IPOs with InCred Money

Continue reading!

The Big Picture

India’s bridal jewellery market runs on a specific tension: buyers want something that is artisanal and ethnic, the production is spread thin across an unorganised cottage industry.

Kundan Polki, one of the most coveted forms of jewellery, is almost entirely handcrafted, and cannot be mechanised. That scarcity creates a structural moat.

Advit Jewels, operating under the brand Rambhajo since 1921, is one of the few organised players in this niche. Based in Jaipur, they make 100% handcrafted jewellery from stunning Polki diamonds and studded jewellery, serving nationwide retailers, regional jewellers and walk-in clients.

They’re now raising funds through a fresh issue of ₹165 Cr. The IPO window is open June 23rd to 25th, 2026. The proceeds will go toward working capital and repayment of bank debt.

Business Model Explained

Advit Jewels makes jewellery the traditional way. Every piece passes through the hands of a karigar, an artisan trained in traditional Kundan techniques.

The company employs 35 karigars in-house, owns the design-to-dispatch process entirely, and does not outsource manufacturing. This keeps quality control tight and margins high.

The business runs on three channels:

B2B: Wholesale to retailers, regional jewellers and family jewellery stores across 18 states. Orders are placed through personal relationships and exhibition-based engagement. Credit terms run 40 to 45 days.

B2C: Walk-in and appointment-based sales at the company’s display centre in Jaipur. Average ticket sizes are higher than B2B, and there is no receivables risk.

Job work: Contract manufacturing for third-party designs. This segment has a low margin, and its share is declining.

How the money flows: The procurement strategy relies on outright purchases and Gold Metal Loan (GML) schemes from authorised banks, while Polki Diamonds and gemstones are acquired via domestic open-market vendors. The company converts these inputs into finished jewellery entirely by hand through skilled artisans and sells at a markup, maintaining a gross margin of ~34% (9MFY26).

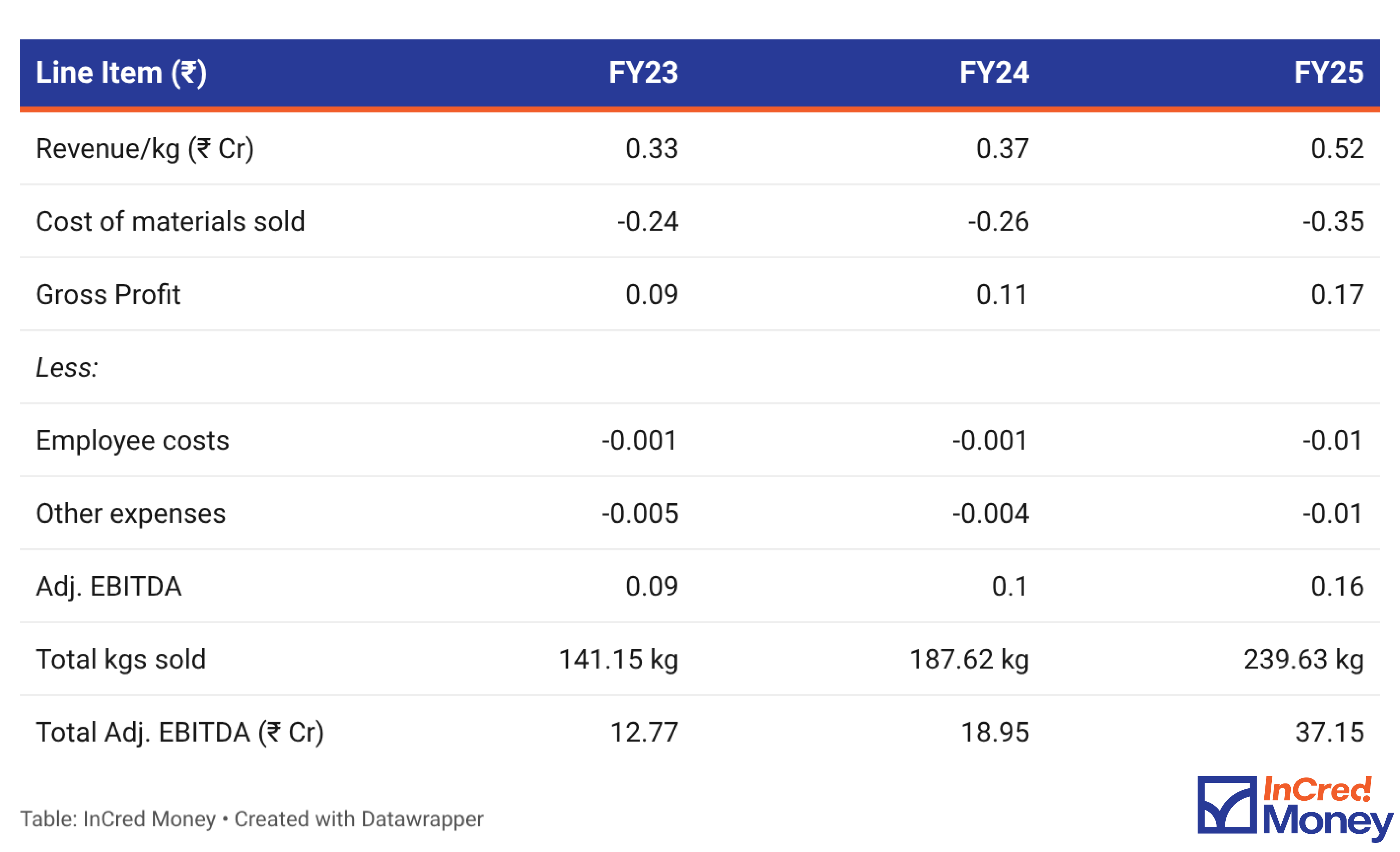

Unit Economics (per kg of finished goods)

On a single kilogram, Advit Jewels earns about ₹17 lakhs of gross profit (FY25), and due to relatively low employee costs and little to none additional expenses, is able to keep most of that, with per kilo EBITDA Margin actually being ~31% in FY25!

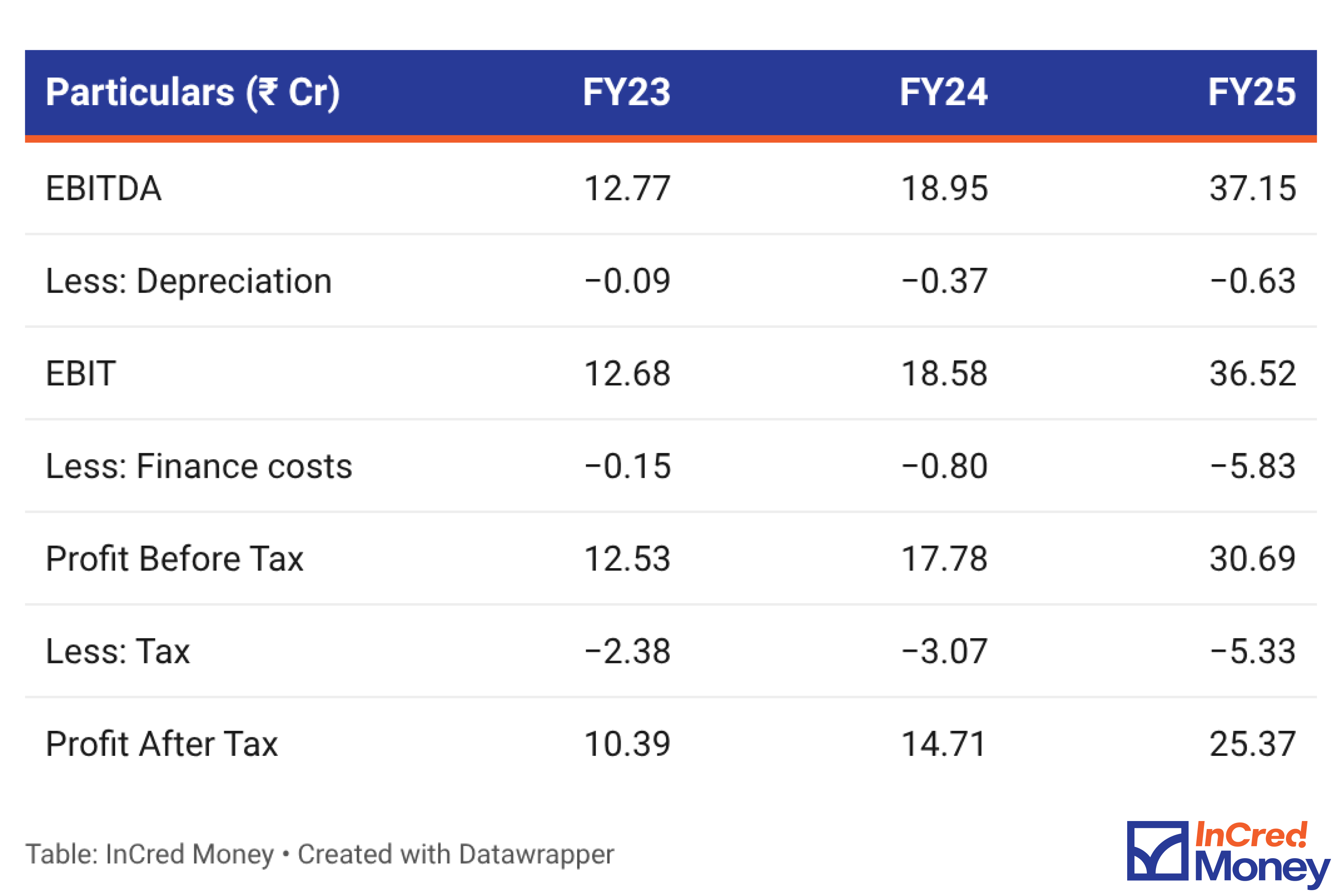

From EBITDA to Net Profit

Working capital loans from HDFC Bank and ICICI Bank amounting to ~₹77 Cr are a big factor in the Finance costs for Advit Jewels in FY25.

Operating Metrics

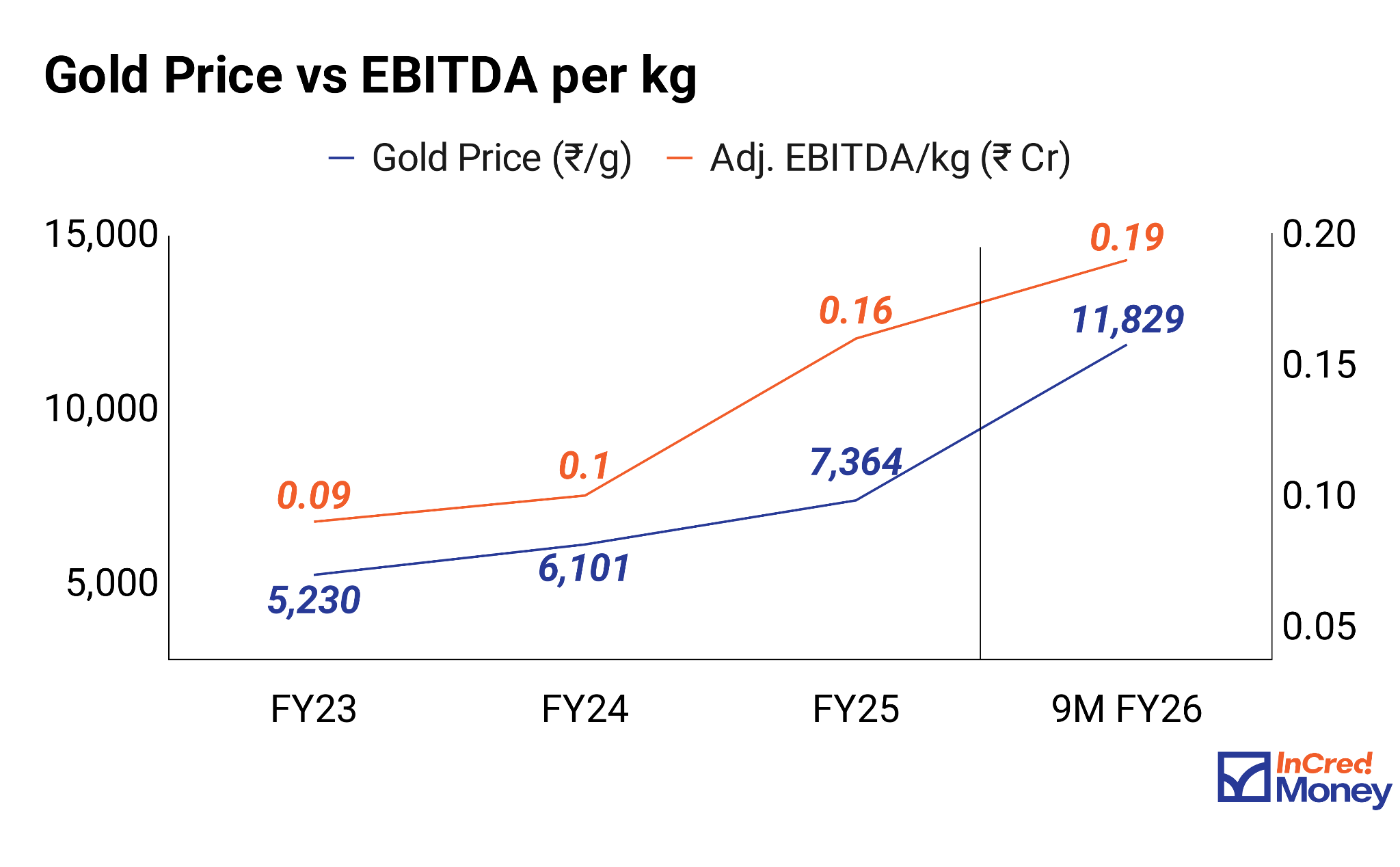

Adj. EBITDA per kg has more than doubled since FY23. The company holds ~200 days of inventory, which means it is selling jewellery made from gold bought six months earlier at lower prices, while realising revenue at current gold-linked prices.

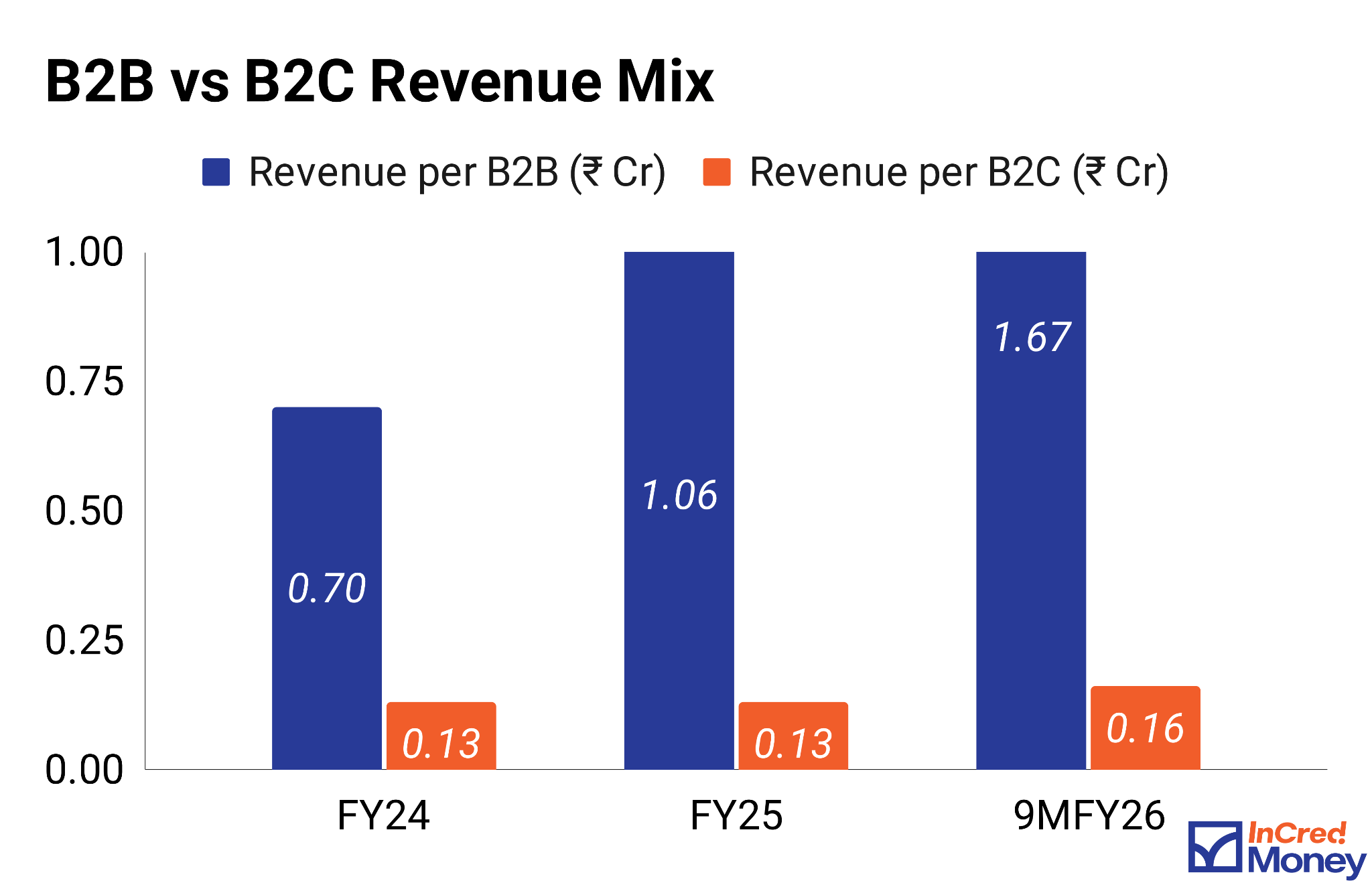

B2B revenue per customer has grown 2.4x from ₹0.70 Cr in FY24 to ₹1.67 Cr as of 9MFY26 (annualising to ₹2.22 Cr). Note that 81% of B2B revenue comes from repeat/existing accounts. B2C revenue has remained relatively flat at ₹0.13 to ₹0.16 Cr. This divergence shows that B2B business is an important growth lever.

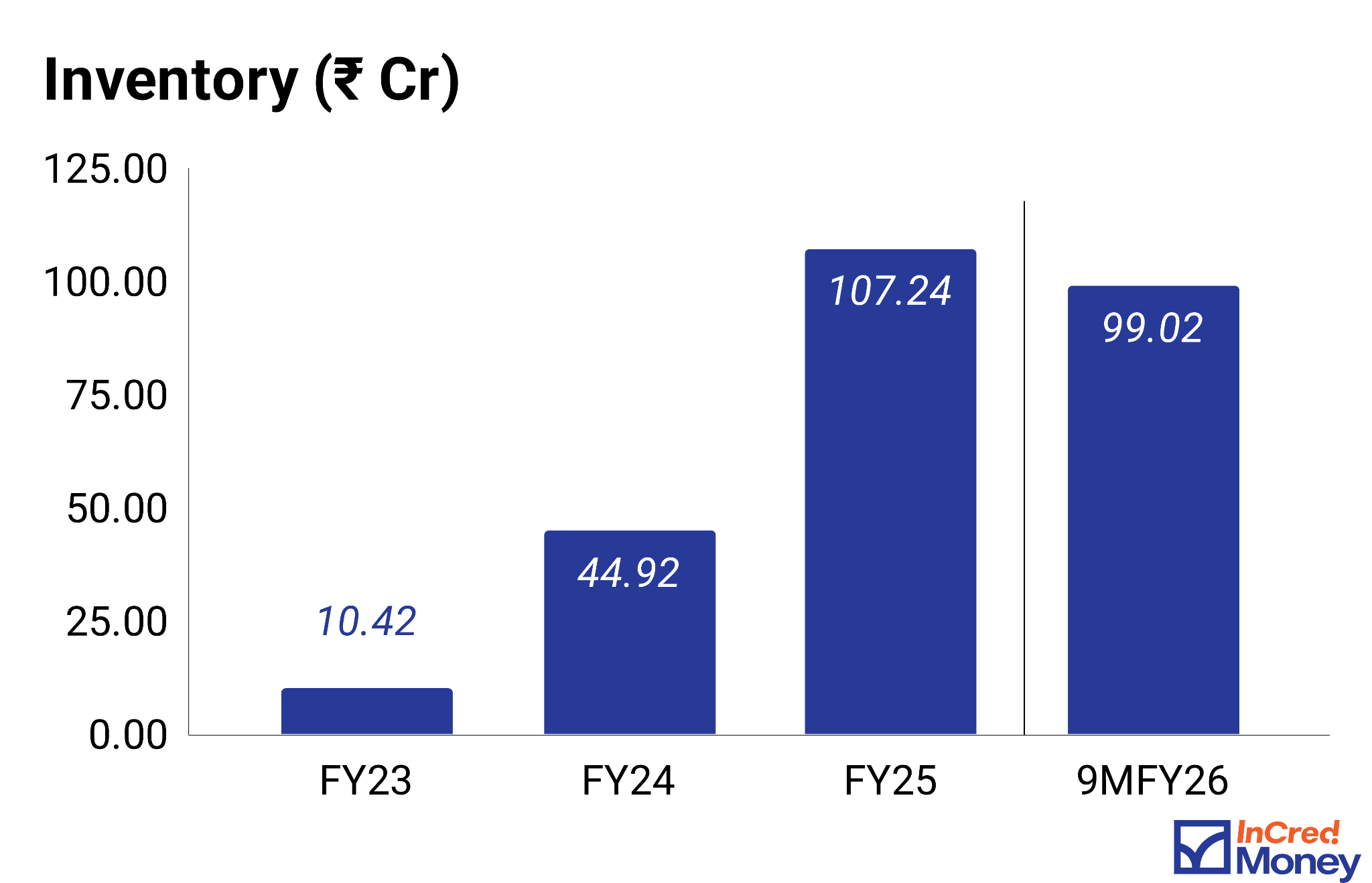

Inventory (consisting of both raw materials and finished goods) has risen sharply from ₹10.42 Cr in FY23 to ~₹100 Cr as of 9MFY26. As gold prices continue to rise, a larger inventory is beneficial as it allows them to sell at a higher margin.

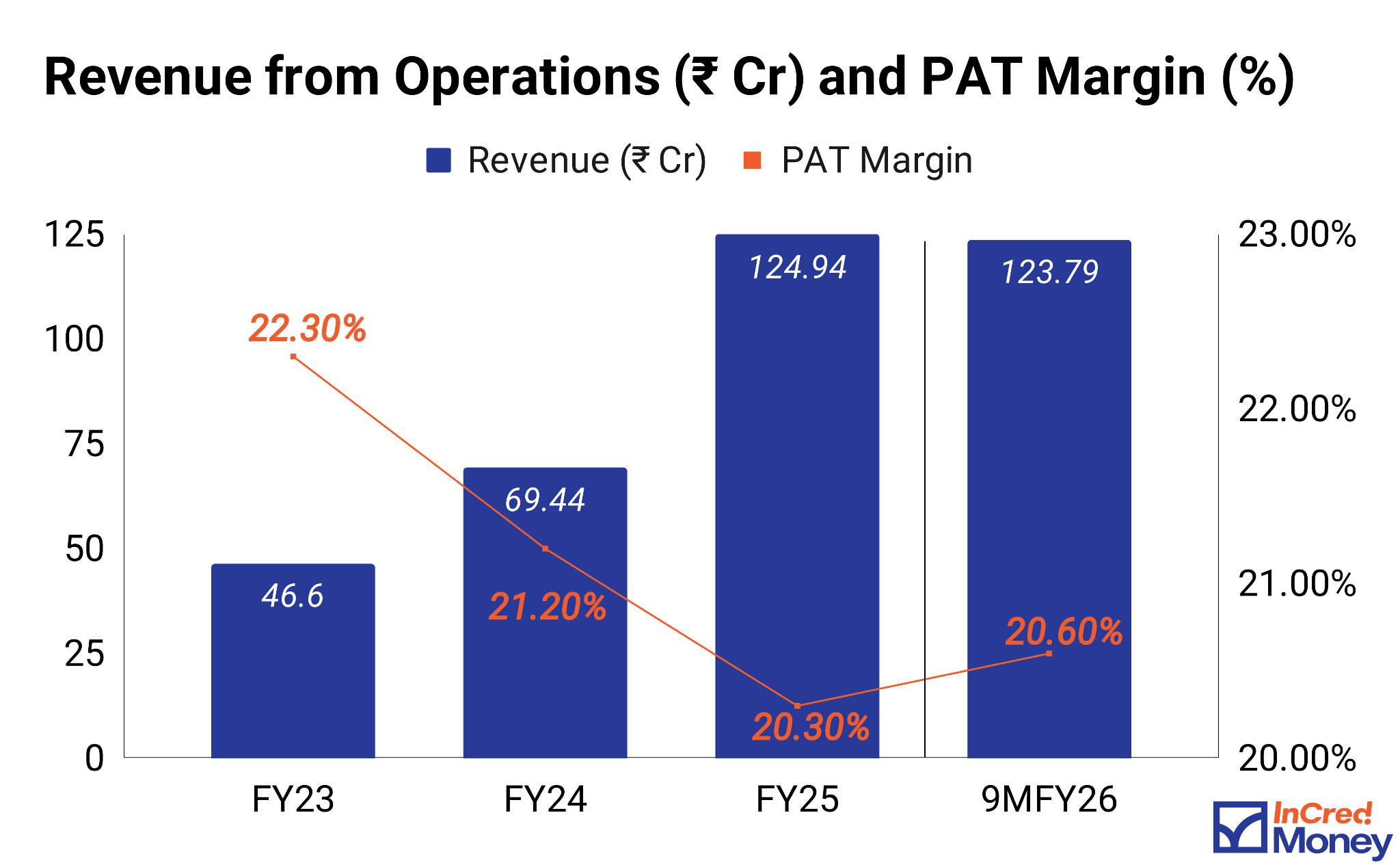

Financial Highlights

Revenue remained flat this year despite customer count falling 26%, meaning that the company is serving fewer accounts at higher values per account, of which B2B sales are an important part.

PAT Margin is also stable, from 22.3% in FY23 to 20.3% in FY25 and 20.6% in 9MFY26. The main lever that will raise margins is Finance costs, once the bank loans are paid off.

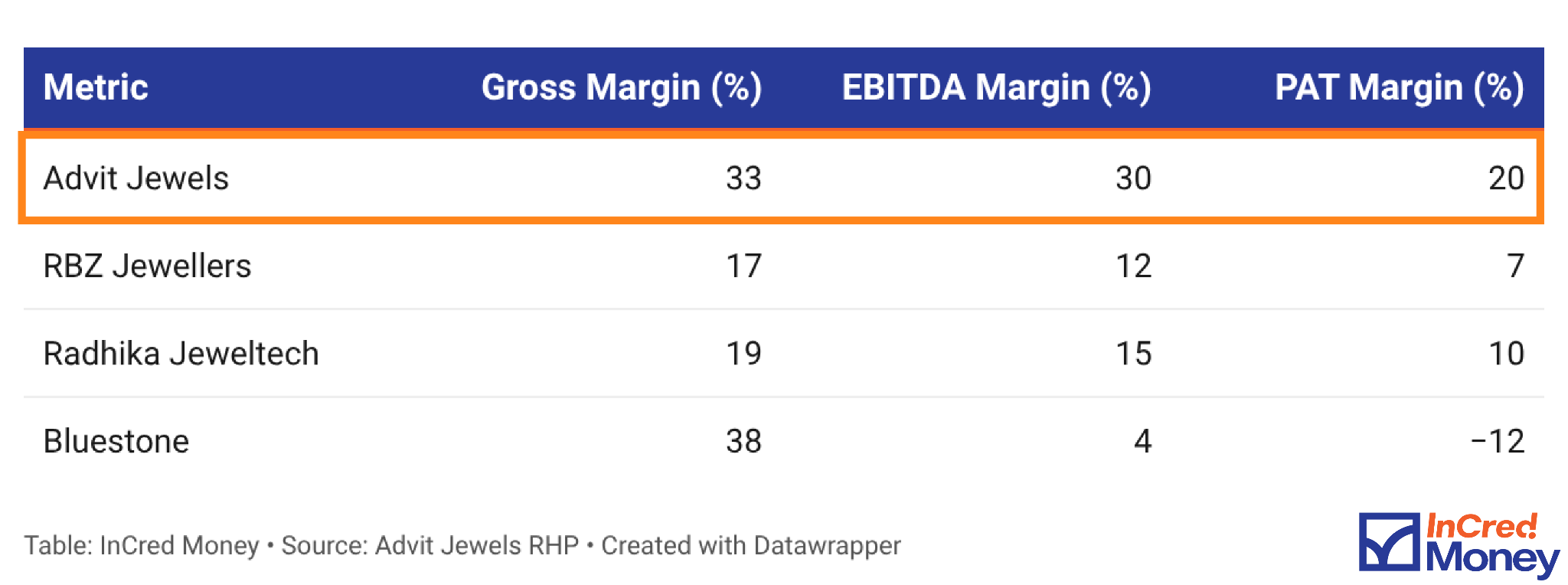

Peer Comparison (FY25)

Advit Jewels’ EBITDA and PAT Margins are by far the highest in the peer set.

Bluestone, despite significantly higher gross margins, generates almost no EBITDA because of its heavy marketing and retail expansion spend.

Advit’s advantage comes from the Kundan Polki specialisation, which commands a premium and faces limited organised competition.

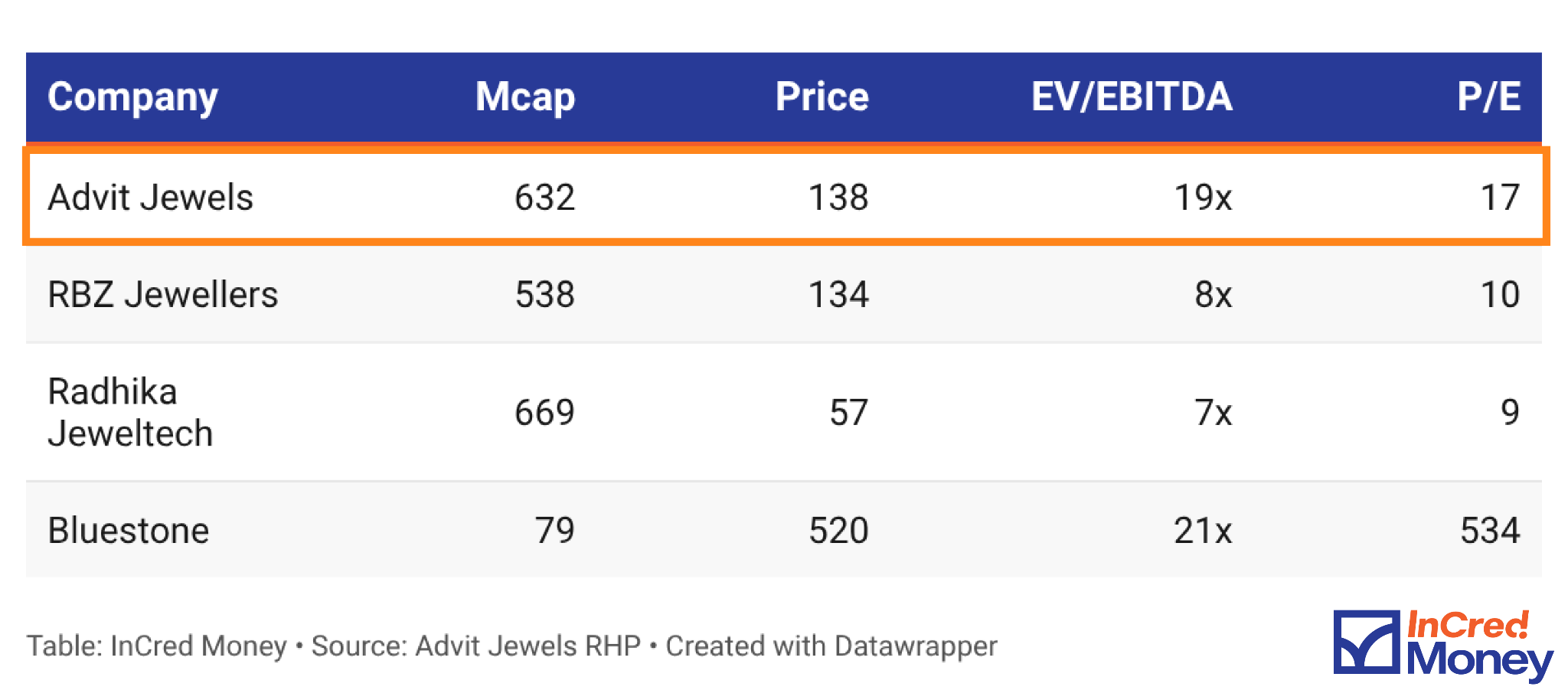

Valuation

Key Risks

Gold Price Exposure: The company holds ~200 days of inventory with no hedging programme. A correction in gold prices would shrink inventory value, and eventually lead to lower margins.

Limited Operating History: Advit Jewels has just six years of operating history, all of which have coincided with a constant surge in gold prices and strong domestic demand. The business has not been tested through a down cycle.

Conclusion

The business Advit Jewels has built is genuinely interesting and the profitability compared to its peers is astounding to say the least. The Kundan niche provides pricing power and limits competition in ways that machine-made jewellery businesses cannot replicate.

If you know someone who might be interested in this IPO, send this article to them today!

Disclaimer

Any video/image/text content is for educational and informational purposes only and does not constitute financial advice. Please do your own research or consult a qualified financial advisor before making any investment or trading decisions. Trading in stock markets involves the risk of loss.

Investments in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

InCred Money Broking Limited : NSE Member Code 09073, BSE Member Code 6329, MCX Member Code: 55215 , NCDEX Member Code : 1233 NSDL : IN-DP-474-2020 . SEBI Registration No. NZ000164738

Compliance Officer: NSE,BSE,MCX,NCDEX,NSDL : Mr RK Jain , 011-40409999 support@stocko.in

Registered Office:- 3rd Floor, Building No.5, Local Shopping Complex, Rishabh Vihar, Near Karkarduma Metro Station. East Delhi – 110092